From Commitment to Covenant: In Private Credit, Structure is Liquidity

Announcing my new working paper: The Covenant Structure of Private Credit Yield

Today I’m happy to share the first draft of a paper that has been both intellectually challenging and deeply rewarding to write: The Covenant Structure of Private Credit Yield: A Contractual Theory of Valuation.

Introduction

In public markets, liquidity is infrastructure-centric. In private credit, it’s contract-derived.

This distinction isn’t cosmetic—it’s foundational. It shapes how capital moves, how yield is generated, and how valuation must be understood. My new paper, The Covenant Structure of Private Credit Yield: A Contractual Theory of Valuation, starts from this basic asymmetry and builds toward a new model of pricing: one in which yield is not discovered through markets, but structured through law.

The paper makes a simple claim with far-reaching consequences: in private credit, yield is not a market-clearing price—it is a contractual output. It is manufactured through a set of covenants that govern when capital may be deployed, recycled, or retrieved. The credit agreement does not merely protect return. It produces it.

This framing matters now because the private credit ecosystem is rapidly evolving beyond origination and hold-to-maturity. A new generation of secondary markets is emerging—GP-leds, LP-leds, credit secondaries—all aiming to trade exposures that were never meant to be liquid. The common approach has been to import the pricing heuristics of public markets: cash flow modeling, spread curves, peer comparables.

But this misses the core fact: liquidity in private credit doesn’t come from pricing infrastructure. It comes from contractual engineering. Exit isn’t found—it is authored. And if secondaries are to scale responsibly, we must first standardize the legal architecture that defines how—and whether—capital can move.

The Covenant-Centric Model of Private Credit Yield

That’s where this paper intervenes. It introduces a fourth valuation model—covenant-centric valuation—to stand alongside the Market, Income, and Replacement Cost approaches outlined in the IPEV Guidelines (2018). Traditional models rely on the assumption that liquidity either exists or can be proxied; they treat covenants as marginal frictions on cash flow. In contrast, the covenant-centric approach begins from the opposite premise: in private credit, covenants are the infrastructure. They determine whether capital can exit, under what conditions, and on whose terms. Yield, then, is not simply a spread over risk—it is the structured output of a liquidity schedule embedded in contract.

While this framework locates the source of value within the so-called “fundamentals” of the asset, it should not be mistaken for a traditional fundamentalist approach. Here, the fundamental is not the estimated cash flows or their timing, but the contractual fundamentals that govern shiftability—that is, the asset’s ability to move through a market structure. In this sense, the covenant-centric model is a hybrid valuation framework: it draws on the specificity of fundamental inputs (contract terms, exposure duration, pacing logic), but reinterprets those inputs through the lens of liquidity engineering and legal design. It treats market structure not as a background condition, but as a design problem to be solved contractually. Value is not discovered through pricing dynamics; it is authored through contract and revealed through structured liquidity.

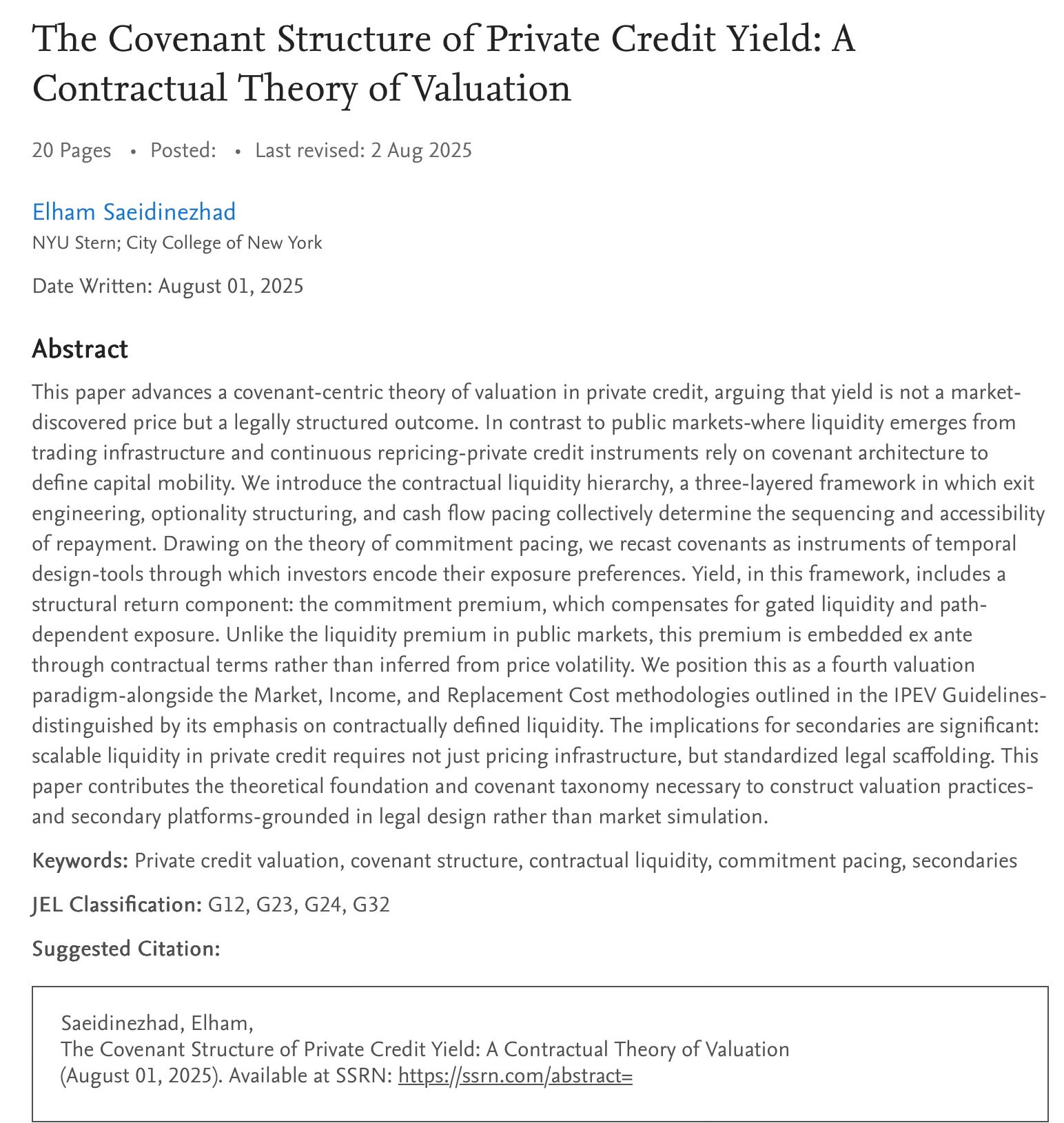

To formalize this view, the paper introduces the contractual liquidity hierarchy: a three-layered model that classifies covenant mechanisms based on their liquidity function. Exit engineering provides legal pathways for capital withdrawal; optionality structuring governs who holds the decision rights over timing; and cash flow pacing sequences repayment across time. These covenant layers collectively shape the investor’s exposure path—not as an incidental constraint, but as the engineered architecture through which private yield is created.

Figure 1- The Contractual Liquidity Hierarchy

The Contractual Liquidity Hierarchy

1. Exit Engineering

At the apex of the pyramid, Exit Engineering contains mechanisms dictating how and when capital can be retrieved. Examples include:

NAV-based resets, where exit is triggered if portfolio NAV falls below a threshold

Take-out rights, where sponsors agree to refinance the lender under specified conditions

Change-of-control clauses, where ownership shifts trigger repayment

Mandatory cash sweep provisions, which accelerate principal return when excess cash exists

These instruments function as synthetic exits. They substitute for secondary sales or refinancing, creating engineered pathways for capital return.

2. Optionality Structuring

The middle layer governs who controls exit timing and on what terms. For example:

Call protections prevent borrowers from repaying early, preserving contractual duration

Prepayment premiums ensure compensation if borrowers terminate early

Equity kickers give lenders upside in exchange for bearing illiquidity

Performance ratchets shift pricing based on borrower milestones

These terms embed liquidity asymmetry—only one party controls the exit, and the other must price in that constraint.

3. Cash Flow Pacing

Forming the base, Cash Flow Pacing gathers instruments that control the sequences of repayment in the absence of tradability. It includes:

PIK toggles, which let borrowers defer interest into principal

Amortization schedules, which pre-structure capital return over time

Step-up/step-down coupons, which align return timing with performance or time horizon

Reinvestment restrictions, which control how returned cash can be redeployed

These covenants define the liquidity timeline, not in response to markets, but as a legal rhythm embedded in the deal.

Together, these three covenant layers are not just risk mitigants—they are functional liquidity modules. They form a hierarchy of covenant liquidity that defines the investor’s exposure path. They determine the capital timeline that, in public markets, would be shaped by hedging, trading, or refinancing. Here, it’s done by design.

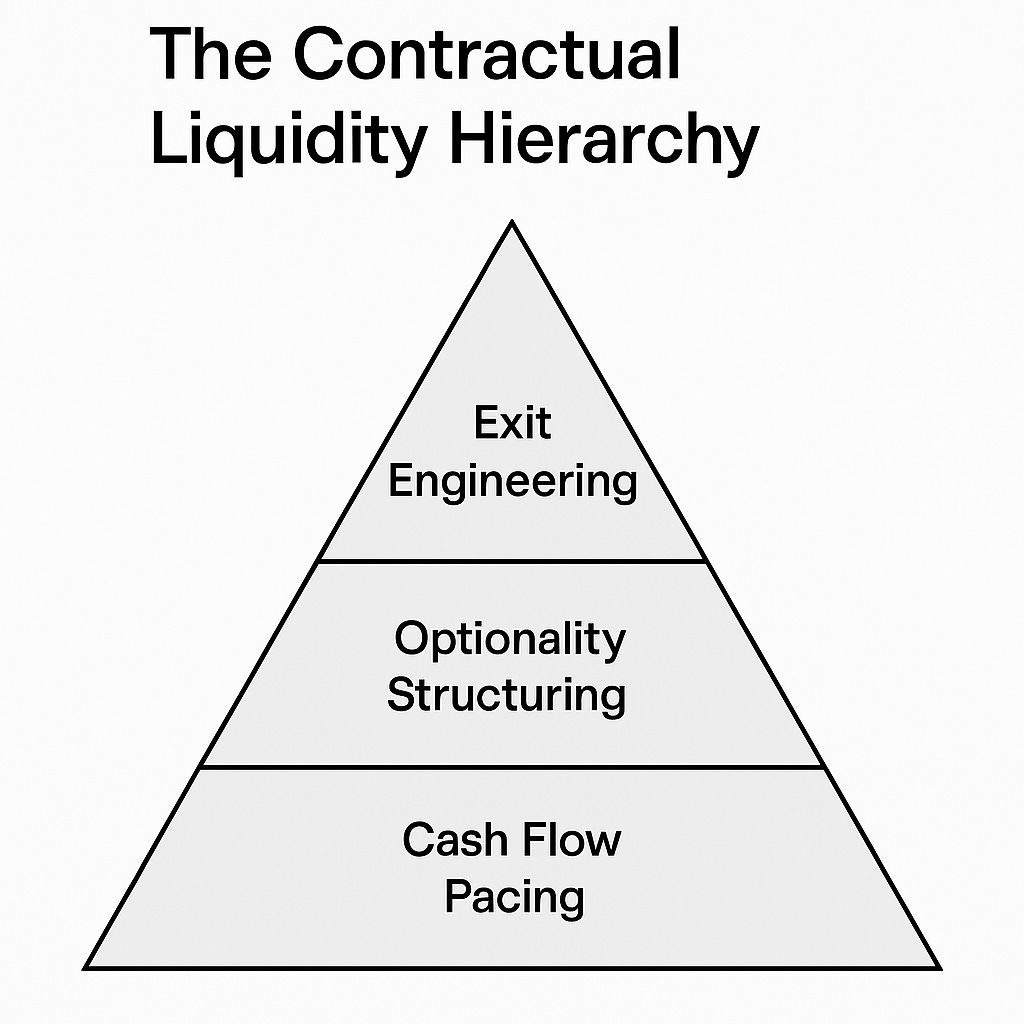

From Fund Pacing to Deal Microarchitecture

This contractual hierarchy does not emerge in a vacuum. To understand how these covenant layers take shape, the paper extends Thomas Meyer’s theory of commitment pacing (Wiley Finance, 2024)—a fund-level framework through which limited partners (LPs) manage illiquid exposure over time by strategically sequencing capital commitments, distributions, and reinvestments across vintages. At that level, commitment pacing is a design solution for managing liquidity constraints, achieving target NAV exposure, and smoothing return volatility.

What this paper contributes is a bridge from that macro-level architecture to the micro-level mechanics of the deal. The central insight is that covenants are not merely negotiated protections against borrower behavior—they are instruments that translate portfolio-level pacing preferences into contract form. Underwriters and lenders do not simply react to borrower fundamentals; they actively shape capital flow through clauses that reflect their own exposure timing preferences, liquidity requirements, and reinvestment logic.

In this sense, the credit agreement becomes a microarchitecture of capital pacing. Where the fund-level model governs how exposure is layered across time, the covenant structure determines how it is sequenced within a single deal. Tools like delayed funding clauses, PIK toggles, reinvestment restrictions, and take-out rights are not just technicalities—they are engineered modules designed to map portfolio strategy onto deal structure. The contract becomes the site where liquidity is not only constrained—but constructed.

Figure 2- Fund and Deal-Level Finance Features

If a lender requires liquidity protection, the credit agreement may include delayed funding provisions or NAV-based reset clauses that trigger early repayment under defined stress conditions. If they aim to extend exposure, call protections or PIK toggles preserve duration. If they’re managing reinvestment pacing, cash sweep redeployment rights or reinvestment restrictions are used to time the recycling of capital.

Each of these covenants operates as a temporal module—an instrument for sequencing capital. They do not merely manage risk; they choreograph return. When assembled into a deal, they form a structured exposure path tailored to the investor’s liquidity profile. The contract does not simply mirror the liquidity environment of public markets—it replaces it with its own internal scaffolding: contractual liquidity.

To illustrating how covenant design encodes liquidity pacing—drawn from common structures in mid-market direct lending deals, consider a $150 million unitranche loan provided by a direct lending fund to a sponsor-backed healthcare services company. The lender—an insurance-backed private credit platform—has known reinvestment pacing constraints: it prefers a 5–7 year exposure, needs semi-annual cash flow for liability matching, and cannot tolerate uncertain capital return near the end of the term.

To align the deal with these pacing needs, the credit agreement includes the following covenants:

Staged Drawdowns: Instead of deploying the full $150 million upfront, the contract specifies a $75 million initial draw, with the remaining capital available in two delayed tranches based on revenue milestones. This gives the lender control over capital deployment timing and limits cash drag.

NAV-Based Reset Clause: If the borrower’s reported enterprise value (via an agreed-upon valuation agent) drops below a 7.5× EBITDA threshold, the lender gains the right to accelerate repayment or force a refinancing. This serves as a synthetic secondary: a contractual exit trigger in lieu of a liquid market.

Call Protection (Soft Call Schedule): For the first two years, the borrower must pay a premium to exit early—3% in year one, 2% in year two. This preserves the lender’s planned duration and protects against premature recycling.

PIK Toggle: The borrower can defer up to 50% of interest payments for four quarters, converting them into principal. This creates temporal flexibility, allowing the lender to remain exposed without needing interim cash—useful if they are managing quarterly liability peaks.

Cash Sweep with Reinvestment Restriction: Any excess free cash flow (above a negotiated capex threshold) must be swept to repay the loan. However, if the lender is still within their reinvestment window (defined as years 2–4), they may re-deploy swept capital into a related acquisition facility. After year 4, the reinvestment right expires.

In this example, the investor’s exposure timeline has been codified in contract. There is no assumption of refinancing, no reliance on an active secondary market, and no pricing of embedded options via observable volatility. Instead, the deal engineers its own liquidity through the careful design of covenants—each chosen to reflect the pacing logic of the capital provider.

This is contractual liquidity, and this is where yield is formed—not in a clearing price, but in a legal structure. As private credit secondaries expand, these pacing-linked covenants will become the key unit of analysis. They must be standardized, disclosed, and eventually priced as modular liquidity instruments.

Why This Matters for Secondaries: Either We Build Synthetic Standards—or Accept That Underwriters Rule

The covenant-centric model has immediate implications for the design and functioning of secondary markets in private credit. As private credit evolves beyond its origin-and-hold foundations, a new generation of secondary transactions—GP-led continuation vehicles, LP-led sales, and NAV-based lending—seeks to introduce liquidity into instruments that were never meant to trade. Yet the dominant pricing approaches on these platforms still rely on heuristics borrowed from public markets: peer comparables, discounted cash flow models, and backward-looking IRRs.

This presents a structural problem. In private credit, liquidity is not an emergent feature of market depth or trading volume. It is not revealed through pricing. Instead, it is encoded directly into the legal structure of the deal. The contract determines whether, when, and how capital can move. This means that yield is not just a reflection of risk—it is a function of liquidity rights designed ex ante.

In this context, underwriters—those who negotiate and structure the deal—are not peripheral actors. They are the core architects of liquidity. Their choices around call protections, NAV triggers, reinvestment restrictions, and amortization schedules define the mobility of capital. As such, the stability or fragility of the secondary market depends not only on pricing infrastructure, but on the cumulative effect of these contractual decisions.

When platforms fail to account for this, they risk treating structurally distinct assets as if they were fungible. Consider the earlier example: a $150 million unitranche loan designed around an investor’s pacing needs. Its NAV-based reset clause, staged draw schedule, and mandatory cash sweep provision effectively create a built-in exit path. The loan can be refinanced or bought out under conditions specified in advance. It functions more like a callable, amortizing bond with contractual liquidity engineered from the start.

Now compare this with a mezzanine loan of the same size and yield that lacks prepayment flexibility, NAV triggers, or reinvestment rights. Though the IRR may be similar on paper, the exposure path is fundamentally different. One offers structured flexibility; the other locks capital in place. Yet without covenant-level analysis, secondary buyers may price them as equivalents.

To address this, secondaries infrastructure must evolve beyond simple price matching and become covenant-aware. This requires:

Mapping exit engineering: identifying the legal mechanisms that permit capital retrieval (e.g., take-out rights, NAV-based resets, change-of-control clauses).

Scoring optionality asymmetry: understanding who holds control over exit and timing (e.g., call protections, performance ratchets).

Analyzing pacing constraints: evaluating how repayment is timed and sequenced (e.g., PIK toggles, amortization schedules, reinvestment restrictions).

The goal is not contractual uniformity. Rather, it is synthetic standardization: grouping assets into comparable liquidity categories based on their legal architecture, not just their pricing profile. In this view, valuation begins not with cash flow projections, but with legal form.

This is not merely a technical improvement—it is foundational to building scalable, credible secondary markets. Without covenant-level transparency and structure-aware underwriting, platforms risk mispricing risk, allocating capital inefficiently, and undermining the legitimacy of private credit as an investable asset class. In markets where liquidity is governed by law, the covenant is the infrastructure.

This is a first draft, and I expect to revise and expand it—especially with empirical validation. But I wanted to share it early, in the spirit of dialogue. Many of the ideas were sharpened through discussion—especially with my phenomenal RA Kai Owen, whose insight and dedication made this process a pleasure.

I’m especially excited to continue exploring:

How synthetic secondaries can be priced via exit engineering,

How pacing metrics can link fund-level exposure targets to deal-level covenant design.

In private credit, the deal is the market—and contractual design is the first principle of value. If secondaries are to scale responsibly, they must be grounded not just in price discovery, but in the covenant logic that governs liquidity itself.