The Covenant Risk Premium: A Framework for Interpreting Private Credit Yield

In effect, private credit returns are not a product of capital market beta—they are a form of contractual alpha.

By Elham Saeidinezhad

This piece emerges from an ongoing research dialogue with my RA, Kai Owen, as we explore the structural foundations of private credit markets. It is part of a broader academic project on the architecture of private capital, and also serves as intellectual groundwork for the HFA–Market Microstructure Symposium, which we are co-organizing at NYU Stern on October 24, 2025.

The symposium will feature two panels dedicated to private capital:

Panel I — Beyond Liquidity, Before Maturity: Closing the Infrastructure Gap in Private Secondaries

Panel II — Silent Partners: Following Banks Through the Architecture of Private Credit

Together, these panels examine how risk, return, and intermediation are being reshaped in private markets—not just through capital flows, but through the evolving microstructure of contracts, infrastructure, and institutional roles.

Executive Summary

Private credit yields more than high-yield bonds—not because the borrowers are riskier, but because the deals are structurally more complex. This paper introduces the concept of the covenant risk premium: the return investors earn for navigating bespoke, non-standardized contracts where enforceability, rights, and remedies vary dramatically.

As private secondaries scale, the market is moving from a liquidity phase—solved with tools like NAV loans and continuation vehicles—into an infrastructure phase, where clearing and standardization become essential. At that point, the key challenge won’t be capital or pricing—it will be understanding what’s actually inside the deal.

The better analogy is no longer “private credit as debt,” but “private credit as derivatives.” Like swaps before them, these bespoke instruments will require shared infrastructure to scale. Without it, the covenant risk premium will remain high—and the market will remain structurally constrained.

In short, private credit doesn’t pay more because it’s riskier—it pays more because it’s harder to understand.

The Covenant Risk Premium: Rethinking Return Drivers in Private Credit

Why do private credit loans yield 200 to 400 basis points more than comparable high-yield bonds, despite exhibiting lower historical default rates and less interest rate sensitivity? The answer, we argue, lies in a hidden but critical return driver: the covenant risk premium.

This premium doesn’t reflect higher credit risk or greater exposure to macro volatility. It reflects the deal-by-deal complexity of private credit lending—the fact that each loan is bespoke, privately negotiated, and governed by covenants that vary widely in structure, enforceability, and transparency. These legal and operational features are not captured by models or ratings. They must be read, understood, and underwritten at the document level. In short, private credit investors are paid not just to hold risk—but to navigate contract complexity.

A Missing Piece: The Microstructure of Covenant Risk

Private credit deals lack the standardization that defines public markets. Unlike syndicated loans or bonds, which come with familiar covenant packages and disclosure templates, private loans are structured case by case. Default triggers, collateral rights, financial reporting terms, and enforcement mechanisms are all negotiated—and often re-negotiated—on a one-off basis.

This idiosyncrasy makes each loan structurally unique. Pricing the risk of a given deal is less about modeling expected loss, and more about understanding whether the lender has real recourse when something goes wrong. There is no off-the-shelf analytics engine for this kind of underwriting. The premium investors demand is compensation for the non-fungibility and opacity of these structures.

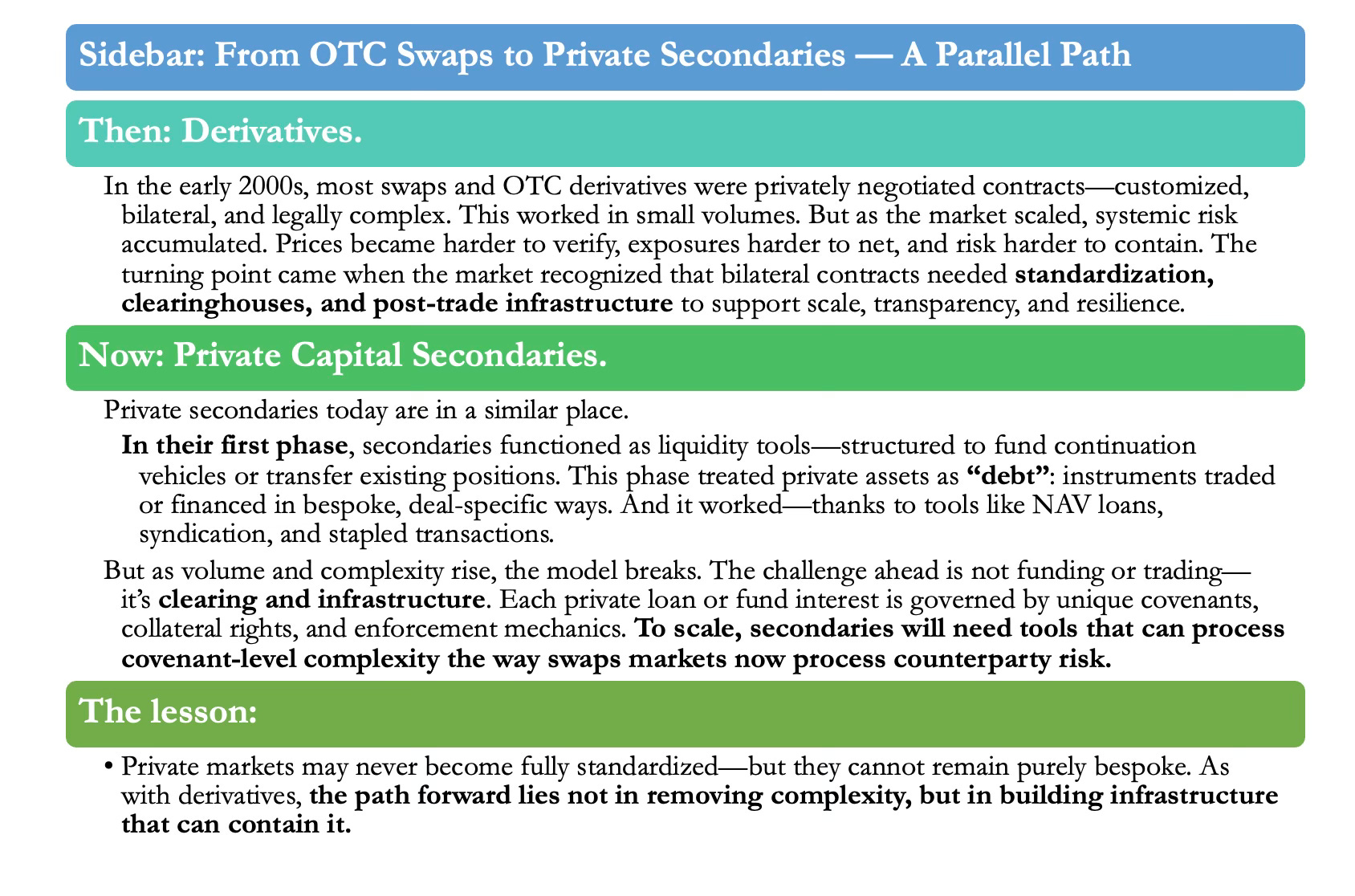

From Liquidity Solutions to Covenant Risk: Secondaries as a Two-Stage Market

This insight also helps illuminate the evolving role of secondaries in private markets. The growing secondaries market has often been framed as a solution to illiquidity—and in its current form, that’s exactly what it is. But the type of illiquidity it addresses is specific.

In what we might call Stage One of secondaries development, the core risks are market illiquidity (the difficulty of selling a position) and funding illiquidity (the inability to raise capital against private assets). The market has developed practical tools to solve both. Syndication, securitization, and continuation vehicles have provided pathways for transferring exposures. Meanwhile, NAV loans, subscription lines, and hybrid facilities have attracted banks and non-bank lenders eager to finance these assets. In this phase, familiar financial engineering techniques have enabled the market to mimic liquidity without requiring deep structural reform.

But Stage Two of secondaries will look very different. As deal flow expands and the market matures, secondaries will increasingly require standardized clearing and settlement infrastructure. That’s when the market will encounter a deeper and less familiar challenge: the covenant risk embedded in these assets. At this point, the relevant question is no longer “Can this asset be bought or funded?”—but rather, “Do we understand what’s inside the deal?”

This is the pivot point where covenant risk becomes central. If secondaries are to scale into a true, institutional market, they will require infrastructure capable of handling the heterogeneity and legal complexity of private loan agreements. Without such infrastructure—whether digital, legal, or administrative—these markets cannot clear efficiently, nor can they price risk transparently.

In this sense, the secondaries market is approaching the same kind of turning point that once reshaped the derivatives market. For years, swaps and other OTC derivatives operated under bespoke bilateral agreements—they were treated, contractually and operationally, as private deals. But once volume, counterparty exposure, and systemic entanglement grew, the industry pivoted toward standardization and clearing, laying the foundation for the centralized infrastructure we now take for granted.

As secondaries shift from solving liquidity to confronting clearing, the better framework is derivatives—not debt. Like swaps before them, bespoke private credit deals must move toward infrastructure that can process legal and structural complexity at scale.

The analogy matters. In the liquidity phase (Stage One), private capital can still be understood as “debt”—a credit instrument that is underwritten, traded, and financed in bilateral ways. But as secondaries grow in complexity and scale, and as we enter the infrastructure phase (Stage Two), the better framework may be that of derivatives: contracts whose value and risk cannot be priced or transferred without understanding their legal structure and institutional ecosystem.

The real bottleneck is no longer liquidity—it is contractual complexity, and the absence of infrastructure to map and manage it. That is what makes covenant risk not just a feature of private credit, but the defining obstacle to the next stage of secondaries market evolution.

Origins in Special Situations Investing

This kind of structural diligence is not new. It has deep roots in special situations investing, where teams were assembled to read complex contracts, map capital structures, and identify overlooked risks in distressed or off-the-run credit. These groups didn’t specialize in forecasting defaults—they specialized in understanding documentation.

Private credit today is, in many ways, an institutionalization of the special situations approach—but with far more capital deployed, and far fewer hours spent per deal. What was once a niche, high-touch activity has become the mainstream engine of private lending, without the institutional apparatus fully evolving alongside it.

A New Name: The Covenant Risk Premium

This reality calls for more than just a better yield model—it demands a new conceptual framework for how we understand return generation in private credit. The excess yield observed in these markets is not, as some assume, a byproduct of traditional fixed-income factors.

It is not a term premium, because most private credit loans are floating-rate and carry minimal interest rate risk. It is not primarily a credit premium in the conventional sense, because default rates—especially in the middle market—are often lower than in the public high-yield universe. And while liquidity risk does play a role, much of it is now engineered around through continuation funds, NAV facilities, and fund-level leverage.

Instead, the defining feature of private credit is its structural complexity. These are not just loans—they are contracts: dense, negotiated agreements with bespoke covenants, variable enforcement rights, uneven disclosure, and legal terms that must be interpreted in context, not just read at face value. And when stress hits, outcomes are driven not by bond math but by how these contracts actually function—who has rights, what counts as a breach, and how quickly value can be defended or recovered.

That is what gives rise to what we call the covenant risk premium: the return investors demand for absorbing structural uncertainty, contractual asymmetry, and documentation friction. It is the premium for underwriting not just financial performance, but legal viability—under stress, in default, and through restructuring. It is paid to those who can decode complexity before it becomes costly.

This premium has several defining features. It is not diversifiable, because each deal is idiosyncratic—defined by its own terms, jurisdictions, counterparties, and negotiation history. It is not easily modelable, because its drivers live in legal clauses, side letters, and operational enforcement mechanics—not in time series data. And it is not always visible, even to those inside the deal, because what matters is not just what is written, but how the pieces interact in practice, especially under downside scenarios.

In effect, private credit returns are not a product of capital market beta—they are a form of contractual alpha. The investor’s edge is not just picking good credits; it’s knowing which documents to trust, which covenants to enforce, and how to do so when the time comes. The covenant risk premium is what bridges the gap between high-yield returns and private credit yields—without relying on worse fundamentals or more market risk.

Recognizing this premium for what it is reframes the discussion not only about pricing and performance—but also about the market infrastructure required to support it. If the primary risk in private credit is embedded in legal structure, then the ecosystem must eventually evolve to track, monitor, and intermediate contractual complexity—just as public markets built tools to manage price volatility and credit risk.

Why It Matters for Microstructure

Understanding the covenant risk premium changes how we think about private market microstructure. It explains why these markets have failed to develop secondary trading platforms despite their size. It clarifies why post-trade infrastructure—from covenant monitoring to compliance tracking—is now critical for sponsors, lenders, and LPs alike. And it helps explain why banks are increasingly involved not just as lenders, but as structuring partners and infrastructure builders.

This isn’t just about capital—it’s about scaffolding. Just as early-stage secondaries used engineering to overcome illiquidity, the next stage will require a different kind of market architecture: one capable of aggregating, tracking, and enforcing covenant-level complexity at scale.

Conclusion

Private credit is often described as a high-yield alternative. But that framing misses what is most distinctive about the asset class. These are not just loans—they are engineered contracts, embedded with custom structures, non-standard covenants, and legally complex terms. The risk premium investors earn is not primarily for taking on macroeconomic or credit risk, but for underwriting structural uncertainty.

This is the covenant risk premium, and it is central to how both private credit and secondaries markets function today. As these markets mature, understanding and managing this premium will determine not only returns—but also the scalability, transparency, and systemic resilience of the ecosystem itself.

References

Cliffwater LLC. 2023 Annual Private Credit Fund Performance Report.

PitchBook LCD. Private Credit Default Rate Benchmarks, 2010–2023.

Preqin. Private Credit Fund Terms and Structures, Q1 2024.

BlackRock Alternatives. Understanding NAV Lending: A Growing Toolkit in Private Markets.

Oaktree Capital Management. Special Situations Strategy Overview, Investor Presentation 2021.

Coller Capital & ILPA. 2023 Global Private Equity Secondary Market Report.

Bank of America Research. Private Credit and the Role of Structuring Banks in the Secondary Market, 2024.

Brookings Institution (Victoria Ivashina & Josh Lerner). The Evolving Role of Private Credit in the Capital Markets, 2022.

SEC Division of Investment Management. Private Funds Advisor Study, 2023.

Duff & Phelps. Valuation Challenges in Illiquid Credit Markets, 2023.